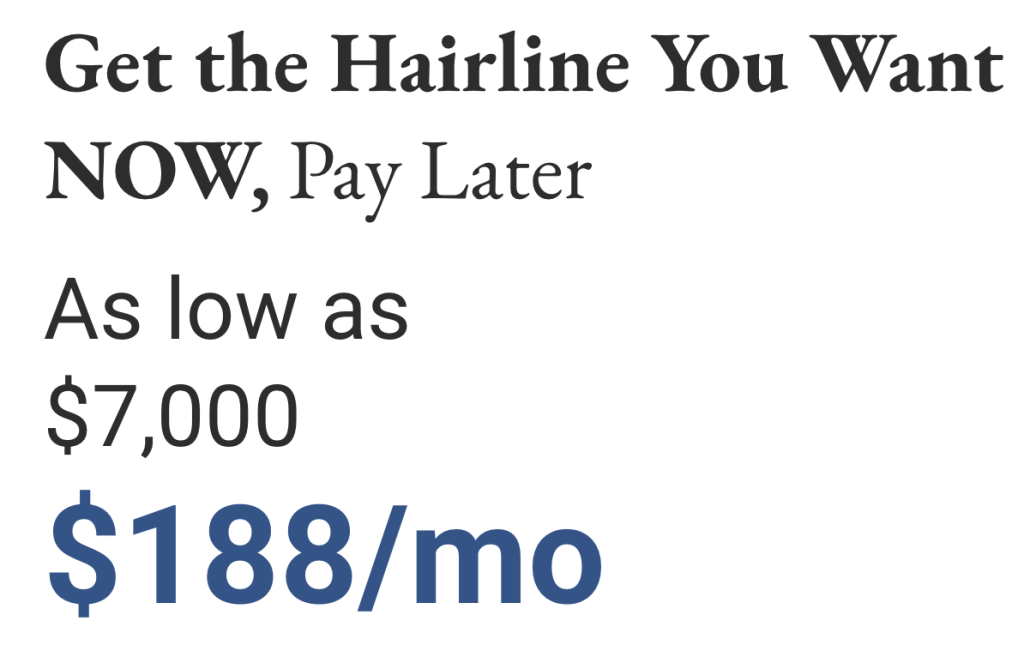

Does your practice advertise hair restoration services with financing options such as “As low as $188/mo”? Then you need to know about an important change Google is making.

For years, lenders such as Cherry, CareCredit, and others have provided a ready-made code to embed on your website or landing pages. They are designed to help you close more opportunities by showing patients how affordable treatment could be in monthly payments. Starting October 28, 2025, that approach may no longer pass Google’s updated Ads Transparency and Misrepresentation policies.

What’s Changing

Google Ads is updating its Dishonest Pricing Practices policy to ensure advertisers disclose the full cost and payment model for any product or service. This includes medical services, elective procedures, and financing offers that promote a partial or teaser price.

Google’s New Requirements:

- Full Cost Disclosure:

You must clearly communicate the total expense a patient will incur, not just the entry-level payment or monthly installment. - Payment Model Transparency:

If your ad references financing or “as low as” pricing, it must also explain the structure of that payment plan (for example: “60-month term at 21.9% APR”). - Prohibited Practices:

Google will deny ads that suggest a cost that doesn’t match the true total, including:

- “Bait-and-switch” style offers

- Hidden auto-renewals or trial conversio

- “Free” offers that require payment to continue

- “Bait-and-switch” style offers

Why It Matters

This policy isn’t just about compliance. It’s about trust. Google’s goal is to help users feel confident that what they see in an ad reflects the real cost of what they’ll pay. That means phrases like “$188/mo” or “starting at $7,000” can’t stand alone anymore without clear context about the terms behind them.

For practices, this will affect:

- Any landing pages using embedded financing widgets.

- Search and display ads that reference price or monthly payments.

- Dynamic landing pages using lender-provided HTML or JavaScript embeds.

While these tools have been provided in good faith by financial institutions in the past, the code itself doesn’t meet Google’s new transparency standards. It only shows the payment amount, not the total cost, loan terms, or APR details in a way Google can verify or read automatically.

Failure to comply with these new Google Ad regulations could lead to account suspension.

What You Need to Do Before October 28, 2025

- Audit Your Ads and Landing Pages

Review any ad or page that mentions a dollar amount. If you’re using “as low as.” Make sure the total cost and terms are also visible in text, not hidden in expandable widgets or lender portals. - Add Full Disclosure Text

Include clear terms such as:

“Payment example: $188/mo at 21.9% APR for 60 months. Total cost $11,453. Subject to credit approval.”

This should appear directly in the ad or on the same page, not just through the lender’s embed info. - Coordinate with Your Financing Partner

Contact Cherry, CareCredit, or your lender to confirm they are updating their code or disclosures to align with Google’s new requirements. - Prepare for Enforcement

Google will begin enforcing this policy on October 28, 2025, with a four-week rollout. If any of your ads violate the policy, you’ll receive a 7-day warning before suspension.

The Takeaway

This is one of those updates that, while easy to overlook, can quietly cause major ad disruptions if ignored. A single non-compliant landing page can hurt your entire ad account’s approval status.

The bottom line:

If you advertise pricing or financing, make sure the total cost, terms, and payment structure are displayed as clearly as your monthly price. This protects your campaigns, maintains compliance, and — most importantly — builds the kind of transparency that earns patient trust.